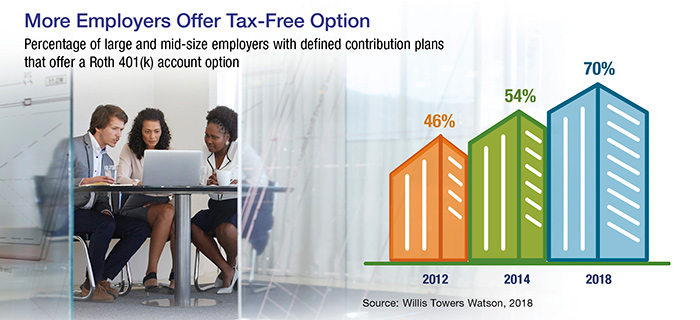

First available in 2006, the Roth 401(k) is a relative newcomer to the retirement savings world, and employers were slow to adopt it. That has changed in recent years. A 2017 survey found that seven out of 10 large and mid-size employers with defined contribution plans offer Roth accounts, and another 15% were planning to add the option or considering doing so (see chart).

A Roth 401(k) is a separate account within the employer’s 401(k) plan that has tax advantages and limitations similar to a Roth IRA. However, 401(k)s have much higher annual contribution limits ($18,500 for all accounts combined in 2018 or $24,500 if you are age 50 or older). And unlike Roth IRAs, there are no income limits for contributing to a Roth 401(k).

If the Roth option is offered in your workplace plan, you might consider its long-term benefits.

Tax Advantage Now or Later

Contributions to a Roth 401(k) account are made with after-tax dollars, so there is no current-year tax advantage. However, distributions — including any earnings — are free of federal income tax as long as they meet certain conditions. Any matching funds from your employer go into a separate pre-tax account and will be taxed as ordinary income upon withdrawal.

Younger workers who are in a lower tax bracket and have many years for potential investment growth may find a Roth account especially appealing. But savers of any age could benefit from tax-free retirement income. When you retire or leave your employer for other reasons, you can transfer your Roth 401(k) balance directly to a Roth IRA, which will allow the assets to continue pursuing tax-free growth. Assets in a Roth 401(k) are subject to required minimum distributions (RMDs) beginning at age 70½, but you are not required to take RMDs from a Roth IRA, which provides more flexibility in managing your retirement income. (Beneficiaries, however, must take RMDs.)

You can contribute to both a Roth account and a traditional account within your employer’s plan, or maintain a balance in one while contributing to the other. If your employer plan allows in-plan conversions, you might convert some traditional 401(k) assets to a Roth account, but be prepared to use funds outside the account to pay taxes on the conversion amount.

Qualified Distributions

Because Roth 401(k) contributions are made on an after-tax basis, they’re always free of federal income tax when distributed from the plan. But any investment earnings on your Roth contributions are tax-free only if you meet the requirements for a “qualified distribution.” In general, a distribution is qualified if it meets a five-year holding period and occurs after age 59½ or after your disability or death.

The five-year holding period starts with the year you make your first Roth contribution to your employer’s 401(k) plan. For example, if you make your initial Roth contribution in December 2018, the first year of your five-year holding period is 2018 and your waiting period ends on December 31, 2022. The start date of the five-year holding period will carry over if you transfer Roth assets to a new employer’s Roth 401(k) plan. Assets rolled to a Roth IRA are subject to the IRA’s five-year holding period.

If your distribution isn’t qualified, the portion of your distribution that represents investment earnings will be taxable and subject to a 10% early-distribution penalty, unless an exception applies.